How Do Social Security Benefits Work?

- zach5896

- Jul 28, 2025

- 5 min read

Summary/TL;DR

The primary variable which determines the value of yours and your spouse’s lifetime Social Security benefits is the age that you claim. Claiming at your Full Retirement Age (FRA), guarantees that you will receive 100% of the benefit that you are entitled to, while permanent penalties and credits are incurred when claiming “early” or “late”. There is no benefit to delaying benefits past age 70. Finally, the unique fashion in which Social Security benefits are taxed renders it vulnerable to a common tax-trap which, unless its proactively planned for, could unnecessarily cost you tens- or hundreds-of-thousands of dollars in retirement.

Introduction

The age at which you and your spouse deicide to claim your Social Security benefits could be one of the most important financial decisions of your life. Understanding the basics of these benefits can greatly mitigate the chances of making mistakes.

This week’s post is dedicated to the basics of Social Security benefits.

Social Security Basics

The exact calculation for determining one’s social security benefits is beyond the scope of this piece, but there are two primary variables: the amount you’ve paid into the system, and your age. The more you’ve paid in, the higher the dollar amount of your benefits will be. Likewise, the older you are when you claim your benefits, the higher they will be.

Your benefit amount will be based on what’s called your Full Retirement Age (FRA), which is in turn determined by your birth year. The FRA for everyone born after 1960 is 67. At this age, you are eligible to claim 100% of your benefit amount. You may also claim as early as 62, but are permanently penalized at a rate of roughly 0.5% for every month before your FRA. Likewise, you may delay your benefits until age 70 in exchange for receiving a permanent increase of roughly 0.67% for every month after your FRA. There is no benefit to claiming after age 70.

Assume, for example, that your FRA is 67 years old and your benefit is $3,500/mo. If you claimed at age 62, you would only be paid $2,450/mo, while if you delayed until age 70, you would be paid $4,340/mo. Recall that these penalties/credits are permanent, so the age that you claim benefits is of primary importance for your retirement planning.

Finally, there is a penalty for claiming benefits before your FRA if you’re still working, although it is not permanent.

Benefits For Spouses

There are two ways that you may claim benefits on your spouse's or ex-spouse’s record – while they are still alive (spousal benefits), or after they pass away (survivor’s benefits). To be eligible for spousal or survivor’s benefits, the marriage must be at least one year old for non-divorced spouses or must have lasted at least 10 years in the case of divorced spouses. If your ex-spouse claims benefits on your record, it does not impact yours or your current spouse's benefits in any way.

Spousal Benefits

The amount of one’s spousal benefits are dependent on two variables: the age at which you claim benefits and the amount of your spouse’s FRA benefit. If you claim spousal benefits at your FRA, you are entitled to 50% of your spouse’s FRA benefit. This 50% rate is applied to your spouse’s FRA benefit, regardless of the age that they actually claim. Like claiming benefits on your own record, there is a permanent penalty incurred for claiming spousal benefits before one’s FRA. You cannot claim spousal benefits until your spouse has claimed on their own benefit.

It is often not advisable to claim on your own benefit first with plans of “switching” to your spouse’s benefits at a later date because of the “deemed filing rule”. The deemed filing rule states that a claim on one benefit is a claim on all benefits that one is eligible for. In other words, if you claim benefits on your record at age 62, perhaps while your spouse is still working and waiting to claim their own benefit, the permanent penalty applied to your benefits will also be applied to your spousal benefits. Because of this, it’s almost always advisable for the lower earning spouse to make no Social Security claims until either their FRA or the age that their spouse claims benefits.

Survivor’s Benefits

The amount of one’s survivor’s benefits are dependent on two variables: the age at which you claim benefits and the age that your spouse claimed benefits. Your FRA for survivors’ benefits is also calculated slightly differently than your FRA for your own benefit, although they will be very similar. If you claim survivors' benefits at your FRA, you are entitled to 100% of the social security benefit that your spouse received while they were alive. This fact makes it a common, and often advisable, strategy for the spouse with the highest benefit to delay claiming benefits until age 70. If your spouse passed away before they were old enough to claim benefits, then your survivor’s benefits will be based on their FRA benefit.

Survivor’s benefits may be claimed as early as age 60, but, as with personal and spousal benefits, a permanent penalty is applied for claiming before one’s FRA. Moreover, survivor's benefits "max-out" at age 67 instead of 70. Finally, the deemed filing rule does not apply to survivor’s benefits. This means you can claim benefits on your own record at age 62 and “switch” to your spouses’ benefits at your FRA for survivor’s benefits with no penalties.

Social Security Taxation

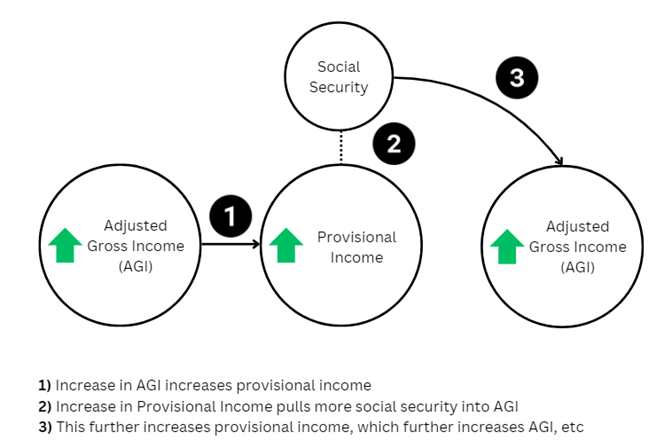

The final “basic” to understand about Social Security is the unique way in which it is taxed. Few people understand that Social Security can be a highly tax-efficient source of income with proper planning. There will never be a circumstance in which more than $0.85 of any dollar you receive from Social Security will be included in your taxable income. What determines how much between 0% and 85% of your Social Security is taxed is determined by your provisional income, which is closely related to your Adjusted Gross Income (AGI). The higher your provisional income, the more of your social security will be included in your taxable income, up to the cap of 85%. The visual below shows how this structure can easily lead to a cycle in which a dollar of additional AGI produces a disproportionately large increase in taxable income.

This is a common tax-trap known as the Social Security Tax Torpedo, which I’ve written in detail about here. Proactive tax planning can help mitigate and sometimes entirely avoid this tax-trap, potentially you tens- or even hundreds-of-thousands of dollars in taxes throughout retirement.