How To Eliminate Capital Gains Taxes

- zach5896

- Jun 17, 2024

- 5 min read

Updated: Jul 18, 2024

Summary/TL;DR

Capital gains tax is incurred when you sell property for more than you sold it for. If the capital gain is considered “long-term”, then it is not taxed according to the ordinary income brackets, but at much more favorable rates. Through the pursuit of strategies such as tax diversification, tax-loss harvesting, and tax-gain harvesting, you can keep your long-term capital gains taxed at a 0% rate, essentially turning your brokerage account into a Roth IRA.

Introduction

Perhaps one of the most misunderstood areas of the US tax code has to do with capital gains taxes. What capital gains are, how they are taxed, and how you can employ savvy tax-planning strategies to eliminate their taxation is the focus of today’s post.

Capital Gains vs Ordinary Income

Ordinary Income

The IRS considers most types of income to be “ordinary income”, and these are taxed at the federal and state income tax brackets. The most common sources of ordinary income are wages, IRA/401(k) distributions, tips, rents, royalties, commissions, interest, pass-through income, and certain types of dividends.

When you file your taxes, all income sources are combined into your “adjusted gross income” (AGI). From there, deductions are made to calculate your taxable income, which is then taxed according to the table below depending on your tax status (single, married filing jointly, etc.) For most people, ordinary income makes up the vast majority of their taxable income.

Capital Gains

A capital gain is income derived from selling property (real estate, stocks, bonds, mutual funds, etc) for more than it was purchased. It is equal to the difference between the net proceeds that the property was sold for and its cost basis (which is often equal to its purchase price). For example, if I purchased a share of AAPL stock in my brokerage account for $100 and sold it for $150, then my capital gain would be $50.

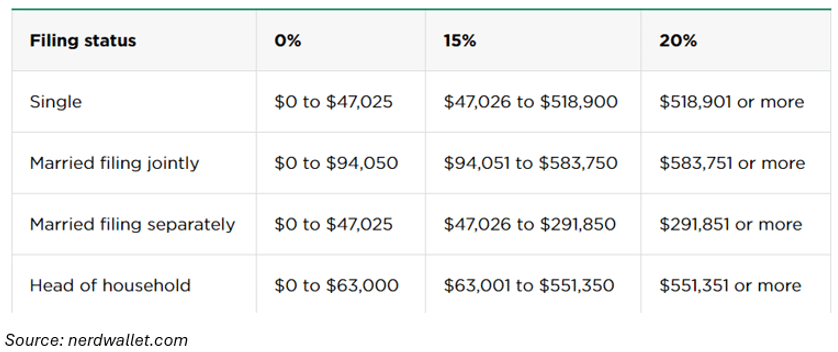

The capital gain tax brackets are much less dizzying than the ordinary income brackets, with only three tiers to keep track of. It’s also important to note that these brackets are based on total taxable income, and not just capital gains (this will be explained in more detail below).

Finally, capital gains can either be considered “short-term capital gains” (STCG), or “long-term capital gains” (LTCG) depending on the length of time that the property was held before it was sold. For holding periods less than one year, the capital gain is considered short-term. Holding periods that exceed one year are considered long-term. STCGs are taxed at the ordinary income level, while LTCGs receive the far favorable tax treatment you see above, with a maximum rate of 20%.

Capital Gains Taxation

When your tax liability is calculated on your return, your taxable income is technically “split up” into its derivative parts (ordinary income and capital gains) and put through their respective tax brackets. For example, if you are a married filing jointly taxpayer and your taxable income is comprised of $100,000 in long-term capital gains and $130,000 in ordinary income, your tax liability would be calculated as follows:

The $130,000 of ordinary income (minus deductions) was taxed according to the ordinary income rates, and the $100,000 of LTCGs were taxed according to the LTCGs rate. Since your taxable income (minus your capital gains) was more than $94,050, all $100,000 in gains was taxed at the 15% rate.

Avoiding Capital Gains Taxation

Tax Diversification

If your taxable income is what determines your LTCG taxation rate, then the key to remaining within the 0% bracket is controlling your taxable income. This is primarily achieved through a strategy called tax diversification, which involves having your portfolio invested across the different types of accounts (pre-tax, Roth, brokerage, etc.).

Having your portfolio invested like this gives you tremendous flexibility in retirement. Instead of being forced to take distributions that are entirely taxable, you can take only as much in taxable distributions as needed for maximum tax efficiency and take the rest from tax-free sources.

To understand how this strategy might work in real life, consider one final example. Let’s assume that you and your spouse are retired and need $100,000 in take-home pay to live comfortably, including your social security:

In this example, you’ve taken a $18,500 distribution from your IRA, a $17,500 distribution from your Roth, and a $10,000 distribution from your brokerage account (for a total of $46,000). When combined with your $54,000 in social security benefits, this totals $100,000 of income. Your annual tax liability, however, is a measly $3!

Tax Loss/Tax Gain Harvesting

Capital gains may be offset by their counterpart – capital losses, which are earned from selling property for less than it was purchased. If capital losses equal capital gains, then capital gains will net to $0 (this has the additional benefit of not adding anything to your taxable income). And if capital losses exceed capital gains in any year, the remainder may be used to offset your ordinary income by up to $3,000 maximum per year. Anything left over after this may be carried forward to future years indefinitely to offset more capital gains or ordinary income.

The intentional realization of capital losses is known as tax-loss harvesting. It works by selling a security and immediately purchasing a different one to simultaneously lock-in the loss and remain invested. When practicing tax-loss harvesting, you must be mindful of the wash sale rule, which says that you may not buy or sell a “substantially identical” security to the one the one that you’ve sold for a loss within 30 days before or after your sale.

Tax-gain harvesting is the intentional realization of a taxable gain that would be incurred within the 0% taxable gain bracket. This effectively resets your cost basis in your property and lowers any potential tax liability in the future. Furthermore, there is no wash-sale rule to have to worry about with tax-gain harvesting. Since there are so many moving pieces to your taxable income (almost all of which are also interconnected), I highly recommend against pursuing tax-gain harvesting on your own.

Leave It To The Kids

The final method for eliminating capital gains taxes is to have your children/grandchildren inherit the property. When a non-spouse inherits taxable property, they receive a “step-up” in its cost basis that is equal to the fair market value of the property on the day that it is inherited, eliminating any capital gains liability for them. It is only growth realized after they inherit the property that is taxable as a capital gain.

For example, suppose you’ve held AAPL stock for your entire life and have a $1,000,000 position composed of $500,000 in cost basis and $500,000 in long term capital gains. When your children inherit the AAPL stock, their cost basis will be “stepped-up” to $1,000,000, meaning they could sell it right away and pay $0 in taxes!

Conclusion

The above strategies are well-known and precisely executed by competent professionals. Attempting to handle this type of complex planning on your own, however, is bound to end in mistakes due to the constant fluctuation of tax legislation and the myriads of other considerations that should be considered in a retirement plan (such as investment, estate, and income planning). This is yet another example of how the cost of working with a financial planner is well below its benefits.