The Most Tax Advantaged Account You Can Invest In

- zach5896

- Aug 12, 2024

- 4 min read

Summary/TL;DR

Health Savings Accounts (HSAs) are available to anyone enrolled in a High Deductible Health Plan (HDHP), either through their employer or the health insurance marketplace. HSAs combine the tax-advantages of Traditional and Roth IRAs to present participants with a triple-tax-advantage that can be extremely powerful when properly used. Finally, when the premium savings of switching to a HDHP are combined with the tax-advantages of HSAs and other employer incentives, many will find that they will save money by switching from switching to an HDHP from a PPO in spite of the higher deductibles.

Introduction

It’s well known that retirement accounts such as Traditional and Roth IRAs have tremendous tax advantages for the patient saver. What’s not common knowledge, however, is that there is an investment account that combines the tax benefits of a Traditional IRA and a Roth IRA without any confusing income phaseouts, making it by far the most tax-advantaged account that one can save into. It’s called a Health Savings Account (HSA), and it can play an extremely powerful and tax-efficient role in your overall portfolio.

Today’s post will therefore cover everything you need to know about Health Savings Accounts.

HSA Basics

Once you understand them, HSAs are relatively straightforward investment vehicles. The only requirement for contributing to one is to be covered by a qualifying High Deductible Health Plan (HDHP). In 2024, this is a health insurance plan with a minimum deductible of $3,200 ($1,600 for single taxpayers) and a maximum out-of-pocket amount of $16,100 ($8,050 for singles). Take note that this requirement is only applicable for contributing to an HSA, but not for using the funds within one. In other words, after you retire and go on Medicare, you can still use the funds you’ve saved within your HSA while you were working to pay for qualified medical expenses (which include Medicare Part A, B, and D premiums).

In 2024, the maximum contribution limit for an HSA is $8,300 ($4,150 for singles), and there is a $1,000 catch-up contribution allowed for taxpayers over the age of 55. In order for married couples to qualify for the higher contribution limits, both spouses must be enrolled in a HDHP. Contributions can usually be made directly out of your paycheck, on a discretionary basis by yourself, or both. And perhaps most importantly, you can claim your contributions as an above-the-line deduction on your tax return regardless of your income!

Once the plan is funded, its assets may usually be invested in just about any publicly traded security that you can imagine. Plan assets will then grow over time and may be distributed tax-free to pay for qualified medical expenses. Any funds used to pay for non-qualifying expenses will be subject to taxes and penalties. However, the penalty for non-qualifying distributions goes away once you turn 65, essentially turning your HSA into a Traditional IRA that is not subject to Required Minimum Distributions.

Furthermore, unlike the also common Flexible Savings Account (FSA), unused funds in an HSA are yours to keep forever. The account follows you from job to job and all throughout retirement. The assets simply remain invested until you decide to distribute them at a later date.

Finally, HSAs are passed tax-free to your surviving spouse who may continue to use the account as you did. Once they pass away and a non-spousal beneficiary inherits the funds, the remaining assets are taxed as ordinary income, although they may be used to pay for qualifying healthcare expenses tax-free within a twelve-month period of inheritance. In the event that no beneficiary is named on your HSA, the account is passed to your estate which in which it is taxed as ordinary income.

The Triple Tax Advantage

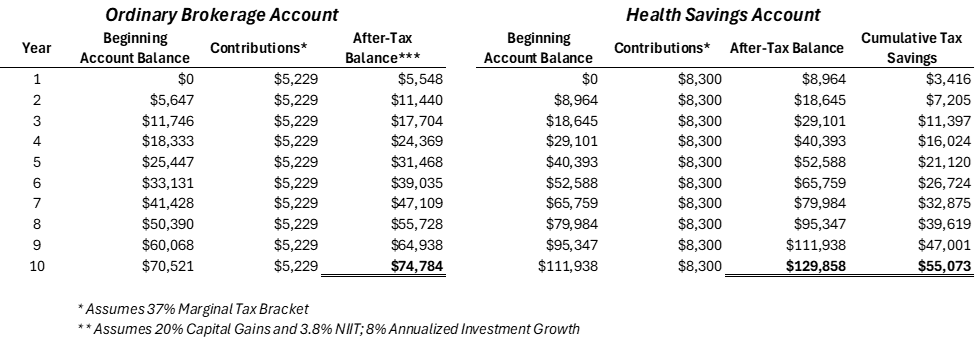

We’ve briefly covered the three tax advantaged characteristics of HSAs – contributions are tax deductible, growth is tax-free, and all distributions are tax-free as long as they are used to pay for qualifying health expenses. In a single year, these advantages aren’t anything to write home about. Over time, however, your tax savings compounds considerably and will result in a well-funded and tax-efficient bucket of savings.

Common HSA Mistakes

The most widespread HSA mistake is to simply not be utilizing it. You might not be contributing because you either don’t know it exists, are unaware of its tremendous benefits, or think that the higher deductible isn’t worth the lower premiums. This section will focus on why this last misconception (that the higher deductible isn’t “worth it”) is almost always completely incorrect.

First, there is the obvious point that you will pay considerably less in premiums throughout the year. Next, recall that your contributions to an HSA are tax deductible, meaning that there’s considerable annual tax savings being left on the table by not participating. If you’re in the 37% tax bracket and make the maximum $8,300 contribution as a married couple, this contribution alone would save you $3,071 in taxes. Finally, your employer would love for you to participate in their HDHP because it’s far less expensive for them, as health insurance is often the most expensive benefit offered by employers. To incentivize their employees to enroll in the company HDHP, many employers will contribute to the HDHP on the employee’s behalf if they choose to participate! This often takes the form of either making a matching contributions or annual contributions of a flat dollar amount.

Taken together, it’s very easy for all of these benefits (lower premiums, tax savings, and employer contributions to the HSA) to exceed the difference in deductibles or even out-of-pocket maximums between your employer’s PPO and HDHP. In other words, you are saving money even if you hit the higher deductible every year which, as we’ve already mentioned, is not likely.

Clearly, a lot of money can be left on the table by not optimizing employer benefits such as company health insurance plans and an HSA. This is exactly where a proactive advisor can play a key role – by reviewing your benefits regularly and breaking down the benefits and disadvantages of every option available to you, they’ll make sure that no stone is left unturned.