5 Costly Mistakes To Avoid In Retirement

- zach5896

- Mar 18, 2024

- 5 min read

Updated: Jul 19, 2024

Summary/TL;DR

Paying no attention to cost, following popular “rules of thumb” for investing, and failing to plan for things such as required minimum distributions, social security taxation, and distribution planning in retirement are all exceptionally common mistakes made by almost everyone. Unfortunately, they are also very expensive mistakes to make. Engaging a competent professional to help you steer clear of any of these, let alone all of them, is worth many multiples of the cost of working with them.

Introduction

Unfortunately, when it comes to retirement planning, the most common mistakes are often the costliest. Avoiding these mistakes, almost all of which are unconscious in nature, usually begins with education – gaining an awareness of their existence and the consequences of ignorance. The solution, in other words, begins with understanding the problem. The aim of this post is to bring the most common of these mistakes, which I also believe will be encountered by almost everyone, to light.

1. Not paying attention to fees

Almost every time I ask someone what they are paying their current advisor, they answer “I have no idea!” And it really isn’t their fault. Fees charged in the financial services industry are often non-transparent and even hidden from customers. Furthermore, they are rarely discussed during client meetings, and any conversations about fees are swiftly shut down or changed to a new topic.

This has cost consumers millions of dollars in fees for services that are offering them negligible amounts of value, and, in many instances, are arguably hurting them. Due to the non-transparent and hidden nature of these fees, consumers will often pay 1.50-2.00% of their portfolio value to their advisor every year. Over time, this seriously adds up. Consider the following example: a $1,000,000 portfolio charged a 1.50% fee will be about $1,000,000 smaller than a portfolio charged no fees over a 20-year period, assuming a 7% rate of return! That is a life-changing amount of money for the retiree, their heirs, or both. By being too nervous to ask about your fees, or too complacent to get a second opinion from an impartial third party, you could really be costing yourself.

2. Being too conservative with your investments

We’ve all heard the following so-called “rule of thumb” – your stock allocation in your portfolio should be 100 minus your age. This is terrible advice. Your asset allocation should have nothing to do with your age and everything to do with your proximity to needing your funds.

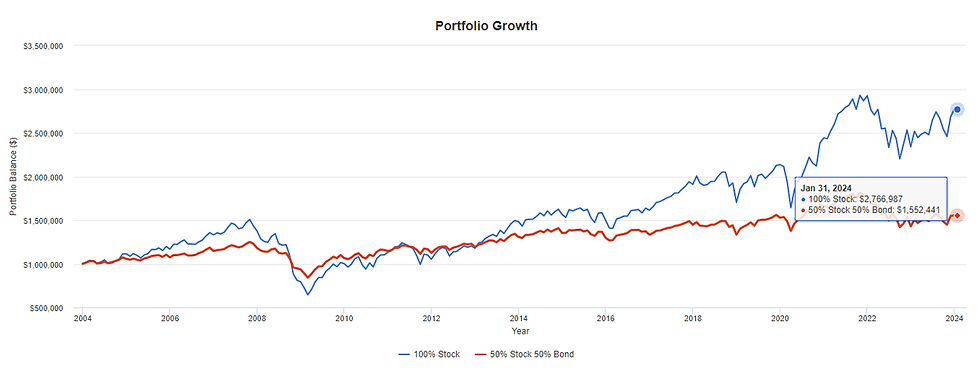

Again, consider the following example. If you retired 20 years ago with $1,000,000 and withdrew $40,000, adjusted for inflation, every year, you would have a portfolio worth about $2,700,000 today even if you stayed invested in 100% stocks! Yes, even after enduring the worst economic catastrophe and stock market crash since the Great Depression in 2008-2009, you would still be far better off. If, however, you felt that being invested in such a stock heavy portfolio was too “risky”, and opted for a 50% stock, 50% bond portfolio, you would only have a portfolio of about $1,500,000.

This does not mean that you should remain invested in a 100% stock portfolio throughout retirement, but it does mean that your “proper” asset allocation is not a function of your age!

3. Not planning for required minimum distributions

Required minimum distributions are forced distributions from pre-tax retirement accounts (such as Traditional IRAs and 401ks) that begin at age 73-75, depending on your year of birth. Of course, taxes are due on these distributions as they are on any distributions from a pre-tax account, and not preparing for them will almost certainly cause far more of your hard-earned wealth to go to the IRS than is necessary.

To see how important this is, consider the following: if you and your spouse retire when you’re 60 with $1,500,000 in pre-tax retirement accounts, your RMDs will be just over $150,000 when you turn 75, assuming the account has been growing at about 6% over that time. If your only income was this RMD, your tax bill would be about $14,000 and you will have paid over $400,000 in taxes just on your RMDs by the time you turn 90.

Not only will not planning for RMDs cause more of your retirement accounts to be taxed than is necessary, but it can also cause more of your social security to be taxed as well! This is known as the social security “tax-torpedo”, and I’ve written about it here.

4. Taking social security too early

Many people are not aware that social security can be some of the most tax-efficient income that you can receive. As such, the more of it that you can receive, the better! Due to a lack of knowledge around how social security is taxed, how it functions, or even concerns about it “going away”, many opt to take their benefits “early” and have it permanently reduced for life. This can be an exceptionally costly mistake.

For every month you claim social security before your full retirement age, your benefit will be reduced by about 0.5%. For every month after your full retirement age that you wait to claim, your benefit will increase by about 0.67%. For example, if your full retirement age is 67 and your annual benefit is scheduled to be $40,000 at this time, you would permanently reduce it to $28,000/yr if you claimed early at age 62. If, however, you waited until your age 70, your benefit would permanently be increased to $49,600/yr!

Not only is your benefit permanently reduced or increased based on the timing of your claim, but the tax-efficiency of social security as an income source is also blunted. The most of your social security benefit that will ever be taxed is 85%, and with proper planning it can be much less. Continuing our example above, if you claim at age 62 and 85% of your benefit is taxable, then $4,200 of your annual benefit would be received tax-free. If you wait until 70 to claim, however, then $7,440 of your benefit would be tax-free, or a 76% increase!

5. Not having a tax-aware distribution plan

Related to the above two points, the order in which you take distributions from your retirement/investment accounts can make a huge difference on your lifetime tax bill. Getting your accounts “setup” for tax diversification will allow you to essentially control your taxable income throughout retirement, opening the door for you to take advantage of more advanced strategies such as Roth conversions and tax-gain harvesting.

I’ve written extensively about this topic here, and a here’s case study about how this type of strategy will help some clients of mine save over $300,000 in taxes over their lifetime.

Again, as discussed above, this type of planning can help you avoid the dreaded social security tax-torpedo. And when used in conjunction with delaying social security benefits, you can easily save thousands in taxes per year. Here’s a table showing three separate scenarios that produce the same amount of net income, but have dramatically different tax consequences:

Conclusion

Sure, if your personal planning strategy consists of scouring Facebook groups, investor magazines, and popular books and radio shows about personal finances, then you’ll likely do better than most. It is impossible, however, to steer clear of every mistake discussed above without the help of a competent professional. Not only do your own circumstances constantly change, rendering the solution to each of these mistakes highly volatile, but so does the legislative and tax environment. Finally, in the same way that making all of these mistakes can be very costly, attempting to “fix” them on your own and making a mistake along the way can prove disastrous.