Can Your Advisor Really "Beat The Market"?

- zach5896

- Jan 13, 2025

- 3 min read

Summary/TL;DR

Research concluding that individuals, even those who can be classified as "professional" investors, consistently fail in their quest to outperform stock market indexes, which investors are able to invest in on their own at essentially no cost. Clients of advisors whose main value proposition is that they will "beat the market" have therefore placed themselves in an awkward situation. Conversely, advisors who don't make empty promises and assist their clients with every aspect of their financial circumstances, especially tax planning, are far more capable of making a genuine impact.

Introduction

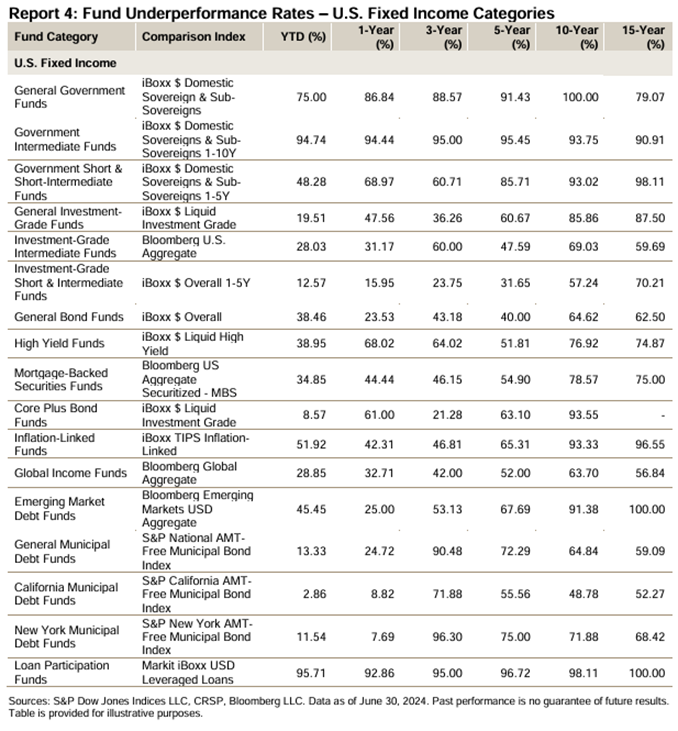

The SPIVA (S&P Indices Versus Active) Report is a research project which tracks the underperformance rate of actively managed funds relative to their benchmarks over various time periods. The latest SPIVA Report, published October 2024, adds to a long history of what has been known to students of financial markets for decades – active portfolio management chronically underperforms passive portfolio management.

In today’s post, we’ll review the results of this report and discuss its implications for those who count on the stock market to grow and preserve their wealth.

The SPIVA Report – Mid Year 2024

Each number in the tables below correspond to the percentage of actively managed funds in a given category (left-most column) that have underperformed their respective benchmarks (second-to-the-left-most column) over the time period listed at the top of the table.

Let’s begin with the most important category – U.S Equities.

Over the past 20 years, 94% of all fund managers have underperformed the benchmarks. In as little as 5 years, this number is almost 86%.

The fund category with the highest rate of underperformance over the past 20 years has been Mid-Cap Core Funds, with 95% underperforming.

The fund category with the lowest rate of underperformance over the past 20 years has been Small-Cap Value Funds, with 87% underperforming

Next, we’ll turn to bonds. While they look to fare better than stocks, their overall results are still quite dismal.

The fund category with the highest rate of underperformance over the past 20 years has been Emerging Market Debt and Loan Participation Funds, with 95% underperforming.

The fund category with the lowest rate of underperformance over the past 20 years has been California Municipal Debt Funds (which I’m sure we all want in our portfolio), with 52% underperforming.

While the year-to-date results for a few categories are slightly higher than average, the overall underperformance rate of all funds is still exceptionally high at over 76%.

The Solution – Index Funds

If it’s extremely difficult and expensive to outperform stock indexes, then the obvious conclusion is to invest directly into the indexes themselves. This wasn’t possible until Jack Bogle, founder of the Vanguard Group, introduced the first index fund into the market – the Vanguard 500 Index Fund. This was arguably the most impactful development in securities markets in modern history, as it allowed investors to access the performance of securities indexes directly, and at very affordable prices. The growth of index funds has been extraordinary, and there is no longer any debate over their superiority to active management.

Investing in index funds alone, however, is also insufficient. The temptation to time the market, over-or-underweight different sectors, sell during a bear market, or invest based on certain “indicators”, still exists within a portfolio of index funds. What’s needed is simple passive ownership. The implication of this research for investors is therefore quite simple – the most reliable way to compound your wealth in the stock market is through passive ownership of index funds. As Bogle himself is famous for saying, “don’t do something, just stand there!”

Why Pay An Advisor?

All of this begs the question, “what am I paying my financial advisor for?” The value proposition of many advisors is related to investment performance. They claim that they can outperform what you could accomplish on your own and will charge a not-inconsequential fee in their attempts to do so. And while this value proposition was potentially valid in past decades, it is clearly antiquated, as the technological innovations made in the securities industry described above have made the magical wealth-creating capacity of the stock markets widely available to everybody for essentially no cost.

The research above suggests, in fact, that advisors who engage in active portfolio management hurt their clients. If advisors serve their clients best by investing passively, then they need to be able to add value in other ways and, fortunately, they can. A good advisor will be well educated not only about portfolio management, but also in retirement, estate, insurance, and especially tax planning. Advisors who are experts in these areas can add tremendous value to their clients by helping them avoid costly and common mistakes.