The Definitive Guide To Roth IRAs

- zach5896

- May 5, 2025

- 5 min read

Summary/TL;DR

Roth IRAs are qualified retirement accounts that allow savers to compound and distribute earnings on their long-term savings 100% tax-free after being opened for at least 5 years and as long as its owner is 59½ or older. Annual contributions to Roth IRAs are limited to $7,000 (plus an additional $1,000 for those age 50 and older) and are reduced to $0 for “high” income earners, although even they can reclaim their ability to make contributions through the “backdoor” Roth IRA. Everyone may convert funds from pre-tax retirement accounts into a Roth, regardless of their income. Inheritors of Roth IRAs are required to distribute funds within a 10-year period, but all earnings will be tax-free.

Introduction

Old and young alike are likely to benefit from the outstanding tax benefits of Roth IRAs, and understanding the rules that govern them is essential to taking full advantage of them.

Today’s post is all about Roth IRAs.

Roth IRA Basics

When funds are deposited into a Roth IRA, they will still be included in your taxable income. However, Roth accounts remain tax-free forever after your original contributions (growth and all) as long as you follow a few IRS rules. Like pre-tax retirement accounts, premature distributions (defined as distributions that take place before age 59½) from Roth IRAs are subject to a 10% penalty in addition to ordinary taxation on growth.

Finally, unlike Traditional IRAs, Roth IRAs are not subject to Required Minimum Distributions (RMDs) while the owner is alive. Funds are allowed to grow in perpetuity, tax-free, for as long as the original account owner lives, and will pass tax-free to their heirs (assuming no estate tax applies).

The 5-Year Rule

Roth IRAs are subject to a 5-year rule which states that they must have been opened for at least 5 years before distributions qualify for favorable tax treatment. If distributions are made before the 5-year period, then taxes (and potentially penalties) will apply on earnings. Contributions in a Roth IRA are always accessible tax and penalty free regardless of age and whether or not the 5-year time limit has been met. The 5-year “clock” will always begin on January 1 of the year that the first Roth IRA contribution is made, regardless of when in the year it was actually completed. Finally, the contribution must be made to a Roth IRA for the 5-year clock to begin – contributions to employer retirement accounts (Roth 401(k), Roth 403(b), Roth 457, etc) do not count.

There are certain cases in which one may take a distribution from a Roth IRA before age 59½ and without satisfying the 5-year rule without paying penalties (although taxes might still apply). These include qualified educational expenses, distributions needed because of disability, or up to $10,000 to pay for a first-time home purchase. A full list of these exceptions can be found here.

Roth Contributions and Roth Conversions

There are two ways that funds can enter a Roth IRA – contributions and conversions. In both contributions and conversions, the destination of the funds is obviously a Roth IRA. What differentiates the two is the source of the funds entering the Roth. In a contribution, the funds that enter the Roth IRA are from a non-qualified account, such as a brokerage account or cash from a bank account. In a Roth conversion, however, the source of the funds are a pre-tax retirement account.

Roth IRA Contributions

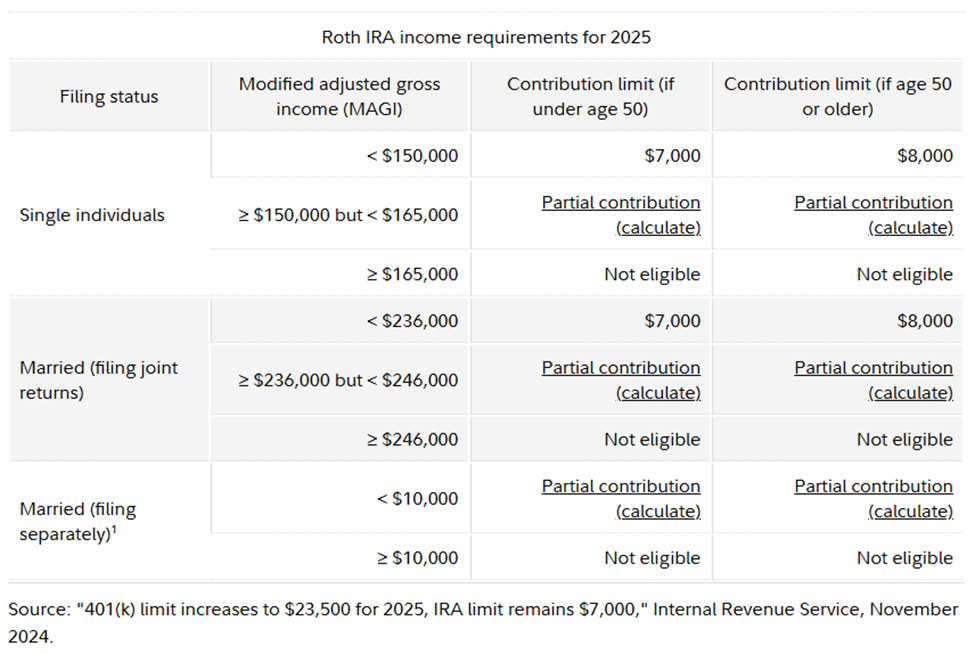

The IRS has placed strict contribution limits on Roth IRAs. In 2025, the annual contribution maximum can be as low as $0 and as high as $7,000 (plus an additional $1,000 “catch-up” contribution for taxpayers over the age of 50). Where a taxpayer falls on this spectrum is determined by their Modified Adjusted Gross Income (MAGI) and is “phased out” as their MAGI grows. The table below shows the income phaseout thresholds for 2025 by tax filing status:

In the example of a taxpayer who is married filing jointly, the income phaseout begins at $236,000 of MAGI and ends at $246,000. This would mean that households with income levels below $236,000 would be allowed the full $7,000 contribution, households with income between $236,000 and $246,000 are allowed a contribution amount less than $7,000 but greater than $0, and households with income above $246,000 aren’t allowed any Roth IRA contributions (unless done via a “backdoor” Roth IRA, which will be discussed below).

Roth IRA Conversions

Unlike contributions, there are no maximums or income phaseouts that plague Roth conversions. Converted funds are taxable in the year they are made, so special care must be taken to ensure that the conversion is tax-efficient.

After making a conversion, taxpayers are faced with two options for paying the taxes: withholding taxes directly from the converted funds, or paying the taxes from a source outside of the Roth IRA. It is essentially always advisable that taxes on a Roth conversion be paid from a source outside of the Roth IRA. Taxes withheld on a conversion are considered distributions and will therefore be subject to the 10% early withdrawal penalty discussed above.

Every Roth conversion is subject to its own 5-year rule that is, unfortunately, quite confusing. The easiest way to understand it is to think of two 5-year clocks, one for taxpayers younger than 59½, and one for those who are older. Those younger than the magic age who distribute any part of their conversion before the clock is up will pay the 10% early withdrawal penalty on the entire distribution, while those older can access converted funds at any time without taxes and penalties. The 5-year rule for those older than 59½ deals with the taxation of earnings on the converted amount, which are taxable until the 5-year period has been satisfied.

Backdoor Roth IRA Contributions

When the difference between Roth contributions and conversions is understood, insight into an opportunity for high income earners to “contribute” to their Roth IRAs is presented through contributing to a Traditional IRA and converting their contribution to a Roth. Because the source of the funds being deposited into the Roth are from a pre-tax account (a Traditional IRA), this transaction qualifies as a Roth conversion and is therefore disallowed to no one!

When making backdoor Roth IRA contributions, you should be careful not to trigger the pro rata rule, which states that distributions from a Traditional IRA will be partially taxable if pre-tax funds in the account are comingled with after-tax funds. Because of this, it is best practice to make the balance of all IRAs you own $0 by December 31 of the year you make the contributions. This can be done by converting all IRA balances to Roth or rolling them over into an employer retirement plan such as a 401(k) or 403(b).

Finally, it is important to file IRS Form 8606 alongside your tax return for any year you make a backdoor Roth IRA contribution.

Inheriting a Roth IRA

Unlike pre-tax retirement accounts, Roth accounts are very tax-efficient to inherit. Any non-spousal beneficiary of a Roth IRA must distribute all funds within a 10-year period, but none of the funds are taxable to the beneficiary. Even in cases of inheritance, however, the 5-year rule discussed above applies beginning in the tax year that the original account owner made the first contribution regardless of whether or not the beneficiary has satisfied the 5-year rule with respect to their own Roth IRAs. Failing to meet the 5-year rule in the case of an inherited Roth IRA will result in earnings being taxed, but there will never be penalties applied.