The Power of Tax Diversification

- zach5896

- May 13, 2024

- 5 min read

Updated: Jul 19, 2024

Summary/TL;DR

Tax diversification refers to having a portfolio comprised of accounts that are taxed in different ways (pre-tax, Roth, brokerage, etc). This strategy affords you an invaluable tool that can be used throughout your retirement – flexibility. Specifically, tax diversification gives you more control over your taxable income and, therefore, your overall tax liability. With careful planning and the assistance of an expert, tax diversification can increase the amount of tax-free social security you receive, allow you to make tax-free Roth conversions, and eliminate capital gains taxes in your brokerage account.

Introduction

Much is made about “diversification” when it comes to asset allocation and investing, but diversification is arguably just as important when it comes to asset location. As you likely know, there are different investment vehicles you can use to save for retirement and the tax ramifications for each type of account differ widely. Most people pick a single vehicle and save into it for their entire lives, completely ignoring the others. This is often a very costly mistake.

Today’s post will focus on the advantages of having your nest-egg spread out across the different types of accounts and some advanced tax strategies available to you through tax diversification.

The Different Types of Accounts and How They Are Taxed

Pre-tax (Traditional) IRAs/401(k)s

If you are retired, I would be willing to bet that most of your investment portfolio is in a “pre-tax” account. This would include Traditional IRAs as well as almost any employer retirement account that doesn’t have the word “Roth” in front of it.

Pre-tax accounts get their name from the fact that funds saved into them are not taxed at the time they are saved. In other words, they are saved before (“pre”) taxation. These funds remain untaxed until they are distributed in retirement, at which point the entire distribution is taxable. Distributions from these accounts become mandatory at age 73-75, depending on your birth year. These mandatory distributions are called Required Minimum Distributions, or RMDs.

Roth IRAs/401(k)s

Roth accounts are just the reverse of “pre-tax” accounts. When funds are deposited into a Roth account, they will still be included in your taxable income. However, Roth accounts remain tax-free forever after your original contributions (growth and all) as long as you follow a few IRS rules.

Non-Qualified Accounts

These accounts get their name from the fact that they are, simply, not “qualified” accounts like the ones discussed above. A qualified account is generally any investment account that qualifies for a tax-advantage contingent on certain rules being followed. A non-qualified account, then, is an account that does not qualify for any tax breaks, but also has the advantage of having no strings attached. Non-qualified accounts are also referred to as “taxable” accounts.

When funds are saved into a non-qualified account, they will still be included in your taxable income. When funds are sold (not necessarily distributed) only the growth is taxable. If funds are sold at a loss, this may reduce your taxes. Generally, if you’ve held the stock for less than a year, the gain will be taxed at your ordinary income rate. If, however, the stock is held for a year or longer, then the gain will either be completely tax-free or taxed at a flat rate of 15% or 20% depending on your overall taxable income.

Being Diversified Across the Different Accounts

One of the most common questions I receive is, “what’s the ‘best’ type of account to have?”. I almost always refer to a financial planning concept known as “tax diversification”, which refers to having a portfolio comprised of all three account types. The heart of the strategy is the flexibility that it affords you when distributing from your portfolio, effectively granting you the ability to control your taxable income. With careful planning, this is one of the most powerful strategies that one can engage in, opening doors to reduce your social security taxation, performing tax-free Roth conversions, and paying no capital gains taxes on your non-qualified accounts.

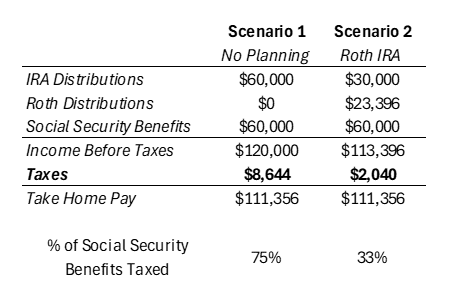

Avoiding Social Security Taxes

Many don’t know that most of their social security benefits will be taxable without careful planning. The percentage of benefits subject to tax is determined by your “provisional income” and could be up to 85% of your annual benefit. Tax diversification gives you more control over your provisional income and, therefore, more control over your tax bill.

Consider the example in the picture below. In the 2024 tax year, a married couple whose only income was $60,000 in IRA distributions and $60,000 in annual social security benefits would have a tax bill of $8,644, with 75% of their social security benefit being subject to taxation. If they were a little more tax diversified, however, they could reduce their provisional income to a level that makes only 33% of their social security benefit taxable and reduce their tax liability by about $6,600 without taking a pay cut!

Tax-Free Roth Conversions

This is one of my favorite strategies to pursue with my clients. If you are properly tax diversified, you can keep your taxable income so low that it falls into negative levels after you take your deductions. This means you can make Roth conversions without incurring any tax liability within a certain range of income!

In the example below, I would pay $0 in taxes despite having $100,000 in take-home pay and making a $16,500 Roth conversion. The implications of this cannot be understated! That $16,500 would remain in my Roth to grow tax free for the rest of my life. If I did this every year for 10 years, I would have converted $165,000 to Roth, paid nothing in taxes, and would have about $697,500 in my Roth IRA for myself, my children, and my grandchildren, to enjoy tax-free after 20 more years of 6% annualized growth. Imagine if we had to pay taxes on that sum!

Eliminate Capital Gains Taxes

For 2024, married couples with a taxable income below $94,300 ($47,150 for single filers) will have their capital gains taxed at 0%. The ability to control your taxable income through tax diversification can, therefore, effectively turn what would otherwise be a taxable brokerage account into a Roth IRA.

Suppose I want to sell $20,000 worth of stock with a $50,000 cost basis and $200,000 in gains. Ordinarily, $16,000 of this $20,000 stock sale would be taxed at a 15% capital gains rate for a $2,400 tax liability. Through tax diversification, I can keep my taxable income below $94,300, sell the same amount of stock, and pay $0 in taxes. Applied to the whole $200,000 gain, this would save me $30,000 in taxes over my lifetime.

Putting It Altogether

While tax diversification can help you pursue any of the strategies discussed above in isolation, it really shines when they are used in combination with one another. Furthermore, to what extent you should be tax diversified depends on your specific circumstances, which means that you shouldn’t pursue tax diversification for its own sake. As always, a knowledgeable and proactive financial planner can help you navigate these complexities, make the right decisions, and, most importantly, avoid costly mistakes.