Million Dollar Mistakes To Avoid In Retirement

- zach5896

- Jun 10, 2024

- 4 min read

Updated: Jul 18, 2024

Summary/TL;DR

The consequences of mistakes, much like the consequences of avoiding them, compound over time. Common mistakes made by retirees, such as not having a tax plan, being too conservative with investments, and not paying attention to fees, will easily compound into seven-figure sums during one’s life. Working with a competent professional who understands your circumstances inside and out can therefore save you a considerable sum.

Introduction

The cost of a financial mistake is not as simple as looking at the dollar amount “lost” or “missed out on”. Instead, the costs of financial mistakes compound because the dollars lost could have been invested and earned a return. Unfortunately, there are many common mistakes whose costs will easily surpass one-million dollars or more, even if they are made relatively late in life. In today’s post, I discuss three mistakes that are routinely made by those who don’t work with competent financial advisors, all three of which will likely cost those making them a seven-figure sum.

Not Planning For RMDs

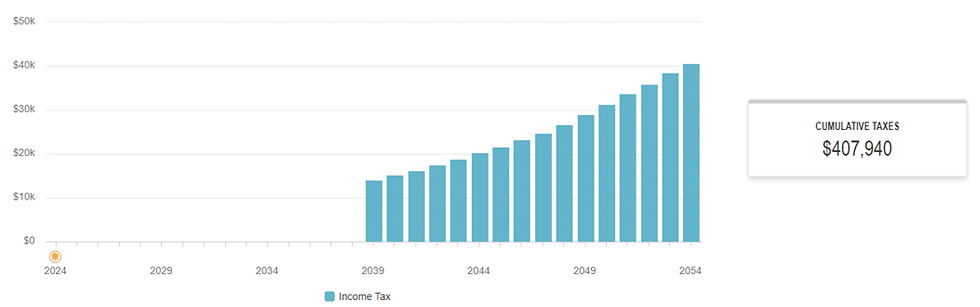

Required minimum distributions (RMDs) are distributions from certain tax-deferred retirement accounts mandated by the IRS beginning between the taxpayer’s age 73-75, depending on their year of birth. In a single year they might not seem like much, but over time they will accumulate to a considerable sum.

For example, if you and your spouse retired at 60 with only $1,500,000 in pre-tax retirement accounts, you would pay over $400,000 in taxes on your RMDs assuming no other income! If these funds had been left in your account to grow, they would be worth almost $1,350,000 by your age 90 assuming 7% annual growth.

There are many things that can be done to prepare for and avoid RMDs altogether, including Roth conversions, qualified charitable distributions, and tax-mindful distribution planning in retirement. When these strategies are planned for well-in advance of RMD age, there is often a lot that can be done to mitigate the cost of these distributions. The longer you wait, however, the less planning opportunities you’ll have at your disposal.

Investing Too Conservatively

Some of the worst advice given to investors young and old has to do with investments. In particular, a lot of lip-service is given to so-called “risk tolerance” and insulating one’s portfolio from volatility. Advice given from this angle is bound to carry conservative biases, resulting in many earning a rate of return far lower than they otherwise could be. Over time, this will easily cost millions of dollars in lost returns.

For example, if you retired 20 years ago with $1,000,000 and withdrew $40,000 adjusted for inflation annually, you would have a portfolio worth about $2,700,000 today even if you stayed invested in 100% stocks! Yes, even after enduring the worst economic catastrophe and stock market crash since the Great Depression in 2008-2009, you would still be far better off. If, however, you felt that being invested in such a stock heavy portfolio was too “risky”, and opted for a 50% stock, 50% bond portfolio, you would only have a portfolio of about $1,500,000.

My preferred approach is to keep 5-7 years’ worth of portfolio distributions in a combination of the money market, short term bonds, and gold, with the rest of the portfolio invested in a diversified mix of stock index funds. For most, this will mean having a portfolio of 70-90% stocks throughout retirement. While this portfolio will certainly be more volatile, the volatility will prove to be short lived and will reward the patient investor with a higher long-term rate of return and a more secure retirement.

Being too conservative will especially hurt young investors who, frankly, have no business owning bonds. Given my “5-7 Year Rule” described above, most people who aren’t retired should have a portfolio of 100% stocks.

Not Paying Attention To Fees

Overpaying fees is one of the most overlooked mistakes out there, not the least because of the lack of transparency and hidden costs in the fee structures of many investment management firms and financial products.

By far the most common fee structure for advisors who manage client portfolios is an assets under management (AUM) fee, which is expressed as a percentage of the client’s portfolio (often 1% or higher). This seemingly innocent fee will compound into a small fortune over time. For example, a 1% fee charged on a $1,000,000 portfolio earning a 7% annual return will be almost $700,000 smaller than a portfolio with no fees after 20 years.

Many advisors will use a tiered AUM structure which decreases as the portfolio size increases. This is typically better than a non-tiered flat fee but can still result in some eye-popping numbers with larger portfolios. AUM fees have the additional disadvantage of being non-transparent. While advisors might be used to thinking in terms of percentages, many consumers are not. Fees should always be quoted and reviewed in terms of dollars and cents.

The final issue with AUM fees is that they present a conflict of interest between the client and advisor. It’s not always in the client’s best interest to have their funds managed by the advisor, and there are many great investments (often real estate related) that require funds to be elsewhere. With an AUM model, the advisor is not compensated on funds that they aren’t managing, meaning that they’re incentivized to discourage their clients from participating in these investments. Furthermore, there might be a lower cost account with similar investments (such as a 401k) that the client would be served just as well in, but the advisor is not likely to be transparent about the cost differences, especially if the rollover opportunity is a large one.

In addition to AUM fees, financial products such as mutual funds or annuities often carry exceptionally high fees, many of which are not disclosed to consumers in an adequate manner. If you thought the example above was egregious, just look at the sales load on an A-shares mutual fund (often over 5%) or the full cost of a variable annuity (which often exceeds 3%).